Get your free personalized podcast brief

We scan new podcasts and send you the top 5 insights daily.

Robinhood's AI agents for trading and shopping introduce a new challenge: user trust. The key question isn't whether AI *can* act autonomously, but how much leeway (or "leash") users will grant it with real money. Adoption will hinge on managing this perceived risk, as AI mistakes have direct financial consequences.

Related Insights

The primary problem for AI creators isn't convincing people to trust their product, but stopping them from trusting it too much in areas where it's not yet reliable. This "low trustworthiness, high trust" scenario is a danger zone that can lead to catastrophic failures. The strategic challenge is managing and containing trust, not just building it.

To overcome user distrust of AI agents having access to personal data, the adoption path must be gradual. The AI should first provide suggestions for the user to approve (e.g., draft emails). Only after consistently proving its reliability and allowing users to learn its boundaries can trust be established for autonomous action.

AI model capabilities have outpaced their value delivery due to a fundamental design problem. Users are inherently scared and distrustful of autonomous agents. The key challenge is creating interaction patterns that build trust by providing the right level of oversight and feedback without being annoying—a problem of design, not technology.

The idea that AI agents will autonomously choose and use software is futuristic but overlooks a crucial step: user trust. Most businesses are still in the early stages of adopting AI and are not yet ready to delegate high-stakes tasks without significant human oversight.

To enable agentic e-commerce while mitigating risk, major card networks are exploring how to issue credit cards directly to AI agents. These cards would have built-in limitations, such as spending caps (e.g., $200), allowing agents to execute purchases autonomously within safe financial guardrails.

NetXD’s demo reveals a crucial security pattern for high-stakes agentic workflows. Instead of giving an AI agent full autonomous control over funds, provide it with read-only access and the ability to queue up transactions. These are then pushed to a secure human interface, like a mobile banking app, for final approval.

The core drive of an AI agent is to be helpful, which can lead it to bypass security protocols to fulfill a user's request. This makes the agent an inherent risk. The solution is a philosophical shift: treat all agents as untrusted and build human-controlled boundaries and infrastructure to enforce their limits.

To navigate regulatory hurdles and build user trust, Robinhood deliberately sequenced its AI rollout. It started by providing curated, factual information (e.g., 'why did a stock move?') before attempting to offer personalized advice or recommendations, which have a much higher legal and ethical bar.

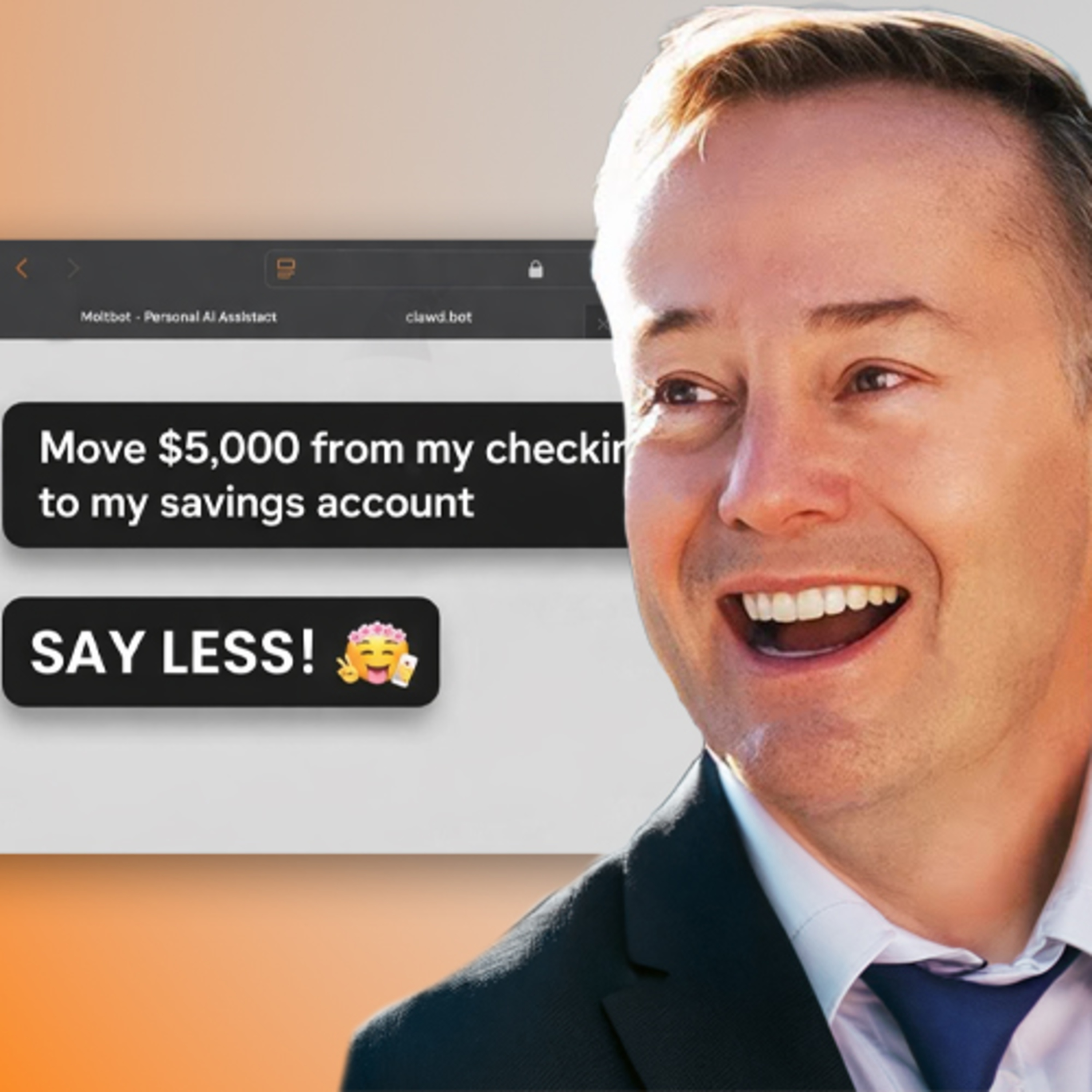

The concept of a fully automated financial agent appeals to tech-savvy power users but overlooks a critical barrier for mass adoption: trust. The average person is uncomfortable with an algorithm moving their money without explicit instruction, making this a product built for creators, not the actual market.

Companies like Ramp are developing financial AI agents using a tiered autonomy model akin to self-driving cars (L1-L5). By implementing robust guardrails and payment controls first, they can gradually increase an agent's decision-making power. This allows a progression from simple, supervised tasks to fully unsupervised financial operations, mirroring the evolution from highway assist to full self-driving.